FinCEN BOI – posted 03.10.25

Please refer to the FinCEN website for the most updated information: https://fincen.gov/boi You are responsible for determining whether you are required to file the BOI and when.

The Corporate Transparency Act (CTA) created new reporting requirements, Beneficial Ownership Information Report (BOI), for companies created or registered to do business in the United States. Effective January 1, 2024, reporting companies will be required to provide information regarding the company and its beneficial owners to the Financial Crimes Enforcement Network (FinCEN). Failure to comply with the new requirements will result in substantial fines and potentially criminal charges. Penalties – see here: Penalties for violating BOI reporting requirements.

Link to FinCEN BOI homepage: This page will always have the most up-to-date information regarding the CTA and BOI reporting.

This is a link to the FinCEN Frequently Asked Questions:

FinCEN BOI Frequently Asked Questions PDF

2 Ways to File

- Directly through the FinCen Website – Free

- Through J. Marc Lewis & Associates – $200

- Click here to file your BOI via J Marc Lewis & Associates

- You will enter your information – payment is due at time of reporting

- Reporting company information, see below

- Beneficial owner information, see below

- We will review your information against our records for your company and submit the report

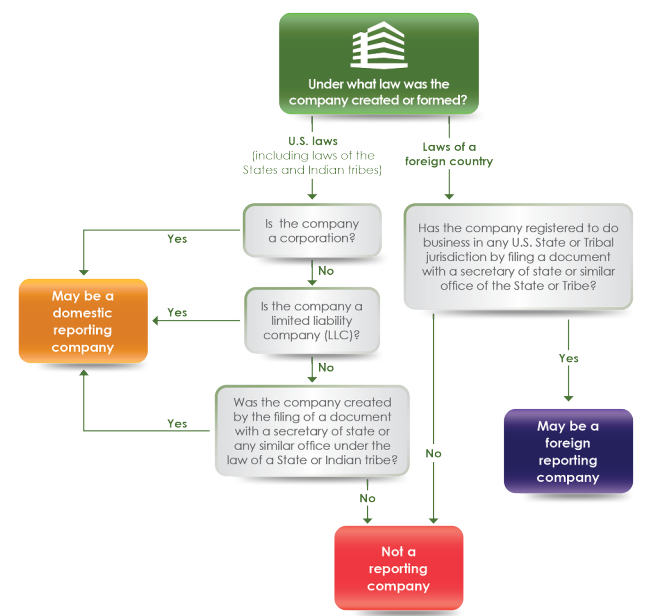

Who Is a Reporting Company?

What companies will be required to report beneficial ownership information to FinCEN?

Companies required to report are called reporting companies. There are two types of reporting companies:

- Domestic reporting companies are corporations, limited liability companies, and any other entities created by the filing of a document with a secretary of state or any similar office in the United States.

- Foreign reporting companies are entities (including corporations and limited liability companies) formed under the law of a foreign country that have registered to do business in the United States by the filing of a document with a secretary of state or any similar office.

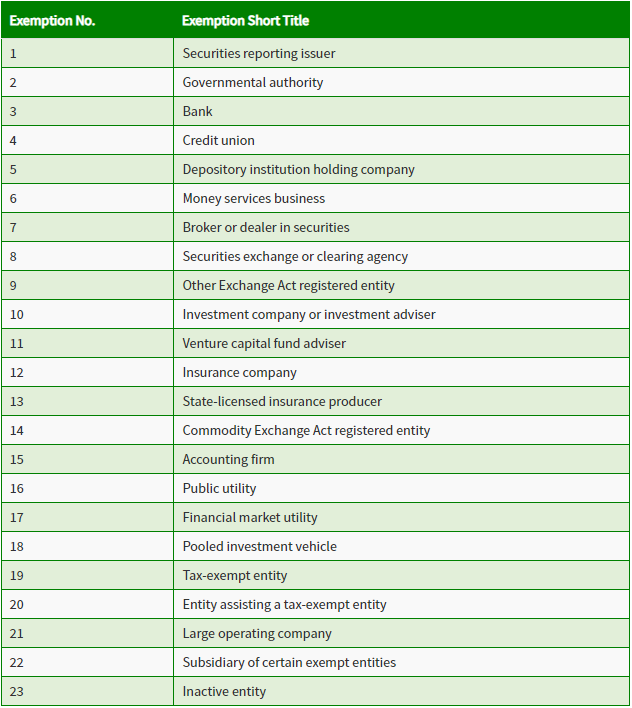

There are 23 types of entities that are exempt from the reporting requirements (see Question C.2). Carefully review the qualifying criteria before concluding that your company is exempt.

Who Is a Beneficial Owner?

FinCEN Who is a beneficial owner of a reporting company?

A beneficial owner is an individual who exercises “substantial control” over the reporting company, either directly or indirectly, or who owns or controls 25% or more of the reporting company’s ownership interests.

Substantial Control

The following individuals are deemed to exercise substantial control over a reporting company:

- A senior officer, such as the reporting company’s president, chief executive officer, chief financial officer, or other high-level officer.

- An individual with the authority to appoint or remove senior officers or a majority of the board of directors or similar body.

- An important decision-maker, more specifically, an individual who controls, directs, determines, or substantially influences important decisions regarding the reporting company’s business, finances, or structure.

- Any other person who exercises substantial control.

Ownership Interest

FinCEN guidance defines ownership interests to include equity, stock, or voting rights; capital or profit interests; convertible instruments; options or privileges; and any other “mechanism used to establish ownership.” An individual who acts as an intermediary, an agent, or a custodian for another may be considered to have indirect ownership.

What Information Must Be Reported?

Beneficial Ownership Information (BOI) Reference Guide – FinCEN

Reporting companies are required to report beneficial ownership information as well as information about the company itself. Reporting companies formed on or after January 1, 2024, will also be required to provide information regarding their company applicants.

Reporting Company Information

Reporting companies must provide the following information about the company:

- The full legal name of the company;

- Any other trade names used by the company; (“doing business as” (dba) or “trading as” (ta) names)

- The street address of the company’s principal place of business (a P.O. box number or third-party address will not be accepted);

- A foreign company that does not have a principal place of business must report the address the company uses to conduct its business in the United States

- The jurisdiction in which the company was formed or registered; and

- An IRS issued Taxpayer Identification Number (TIN).

- Foreign reporting companies without a TIN must report a tax identification number issued by a foreign jurisdiction and identify the issuing jurisdiction.

Beneficial Owner Information

Reporting companies must provide the following information about their beneficial owners:

- Full legal name;

- Date of birth;

- Current residential or business street address;

- A unique identifying number from a non-expired, government-issued photo ID, such as a U.S. passport or state driver’s license (a foreign passport will be accepted if no U.S. issued ID is available); and

- An image of the government-issued photo ID from which the number was provided.

Company Applicant Information

A reporting company that was created on or after January 1, 2024, must identify at least one, but no more than two, company applicants. Company applicants must be individuals, and the same information must be provided for company applicants as is required for beneficial owners.

There are two types of company applicants: a direct filer and an “individual who directs or controls the filing action.”

- A direct filer is the individual who physically or electronically filed the document that created a domestic reporting company or registered a foreign reporting company with the secretary of state.

- The “individual who directs or controls the filing action” is the individual who was primarily responsible for directing or controlling the document that created or registered the reporting company.

If a reporting company has one individual who directly filed the document and another individual who controlled or directed the filing, both individuals must be identified.

FinCEN Identifier

Reporting companies, beneficial owners, and company applicants will have the option to obtain a unique identifier from FinCEN. Individuals who apply for a FinCEN identifier must provide the same information that would be submitted for beneficial owners and company applicants. Reporting companies may report a FinCEN identifier in lieu of the required information about beneficial owners and company applicants. A reporting company may apply for a FinCEN identifier by checking a box on the BOI reporting form.

Filing the Report

Reporting companies will be able to file reports beginning January 1, 2024. Reporting companies in existence prior to January 1, 2024, must file their reports by January 1, 2025. Reporting companies created on or after January 1, 2024, will be required to file a report within 30 days of the earlier of the date of creation or registration with their governing jurisdiction. If there is a change to the reported information, reporting companies must submit updated reports reflecting such a change within one year.

Reporting companies will be required to file their reports electronically through the beneficial ownership secure system (BOSS) created by FinCEN. The system will not be available until January 1, 2024. FinCEN has advised that further instructions and guidance on how to complete and file the BOI report form will be released in the future.

Penalties

Penalties for violating BOI reporting requirements

Willfully providing false information or failing to report or update beneficial ownership information may result in significant penalties. The civil penalty for a violation is $500 per day, while criminal penalties include fines of up to $10,000, imprisonment for up to two years, or both. If a report is filed that contains inaccurate information and the reporting company did not have actual knowledge the information was incorrect, it will be given a 90-day safe harbor to submit an accurate report.

The CTA’s reporting requirements will impact many companies and will likely require a significant amount of information gathering and analysis. We recommend that you consult with your legal counsel to determine your reporting obligations.